2024 New York City Area AMI

2024 New York City Area AMI How do I use this chart? Find your family size in the left column. Follow that row across until you find how m...

Blog about NYC real estate by NYC Broker Mitchell Hall. Homes, architecture, neighborhoods, new developments, market reports, trends and more...

2024 New York City Area AMI How do I use this chart? Find your family size in the left column. Follow that row across until you find how m...

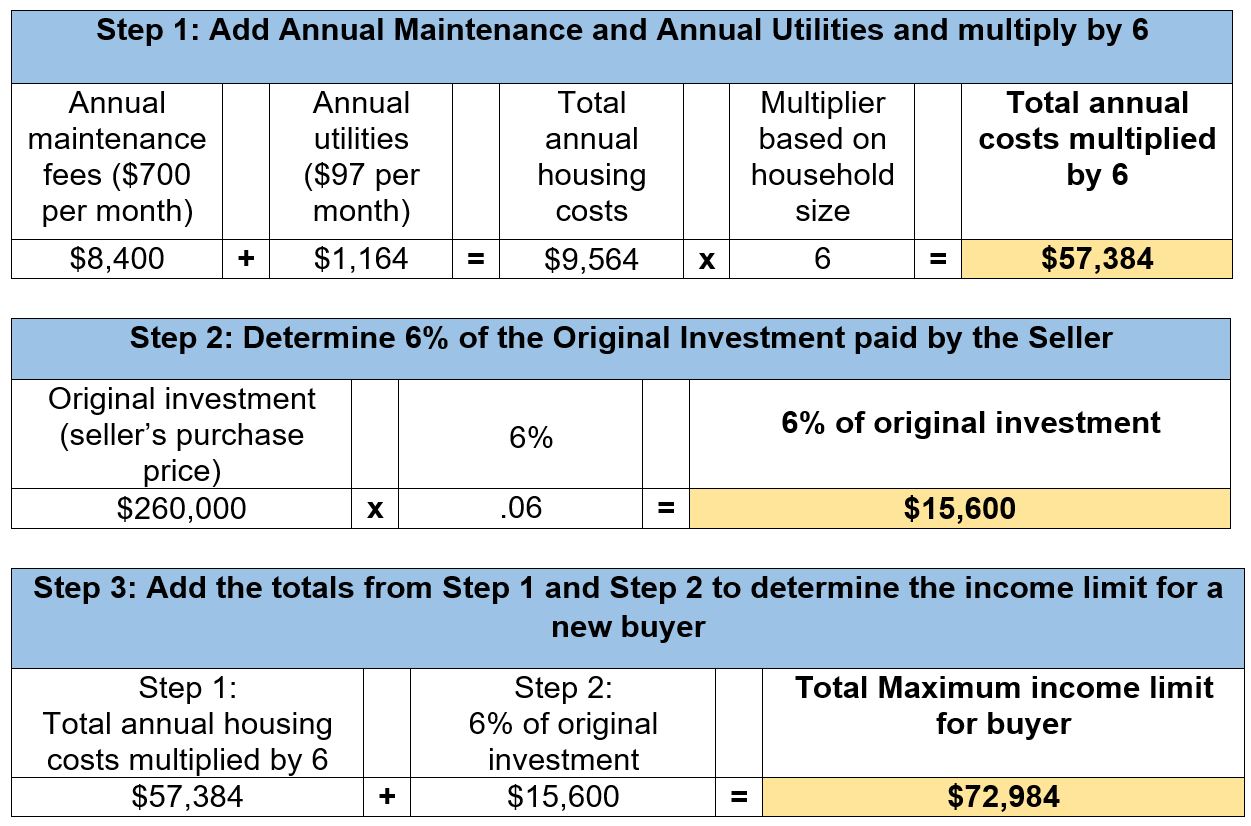

All HDFC coops are incorporated under Article XI and must comply with its requirements. Article XI requires HDFC coops to provide housing fo...

The HDFC community is facing a new threat from City government, and the HDFC coalition needs your help to win. HDFC shareholder/owne...

Why sell your HDFC coop now? As an industry recognized expert in HDFC coop sales, I've been asked by buyers, sellers and HDFC coop b...