Parents Buying - Guarantors and Co- purchasing

Over the years I have sold and rented apartments where a guarantor was needed . I have also sold apartments where parents and/or trust ...

Blog about NYC real estate by NYC Broker Mitchell Hall. Homes, architecture, neighborhoods, new developments, market reports, trends and more...

Over the years I have sold and rented apartments where a guarantor was needed . I have also sold apartments where parents and/or trust ...

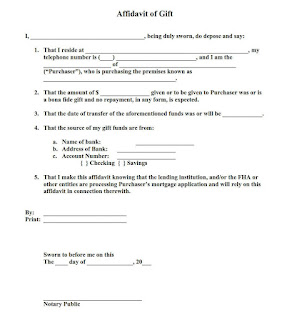

Co-purchasing, Gifting, Guarantors Many first time home purchasers are fortunate to get help from their parents. There are several wa...

What are Guarantors Co Signers and Co-Purchasers? Over the years I have sold and rented apartments where a guarantor was needed . I ha...

In a condo it is very simple. A parent can buy for an adult child. A corporation and or a trust can buy a condo. Some condos have appli...